Topic 4.1 - Individuals, firms, markets and market failure

![AQA ECONOMICS A-LEVEL SPECIFICATION SYLLABUS TOPIC 4.1 [THE OBJECTIVES OF FIRMS]](https://images.squarespace-cdn.com/content/v1/55b690f2e4b076db679cd340/682cd916-b0e6-4266-b063-045ebf7b003d/AQA+ECONOMICS+A-LEVEL+SPECIFICATION+SYLLABUS+TOPIC+4.1+%5BTHE+OBJECTIVES+OF+FIRMS%5D)

Snapshot of the AQA syllabus topic area we’ll be covering in this post.

the objectives of firms: Perfect competition, imperfectly competitive markets and monopoly

AQA students must understand the following content [taken from the syllabus]

The models that comprise the traditional theory of the firm are based upon the assumption that firms aim to maximise profits.

The profit-maximising rule (MC=MR).

The reasons for and the consequences of a divorce of ownership from control.

Firms have a variety of other possible objectives.

The satisficing principle.

INFORMATION YOU NEED TO KNOW

[NOTE: supporting diagrams at the end]

Introduction:

Companies in the world today aim to achieve more than just profit maximisation. The profit-maximizing rule, the separation of ownership and control, alternate purposes, and the idea of satisficing are all covered in further detail on this page about the goals of businesses. We also look at the particular circumstances that businesses must meet in order to accomplish goals like maximising sales income.

1. Profit Maximisation:

According to the classic idea of the business, firms want to make the most money possible (profit maximisation). This goal entails determining the optimal output level at which marginal cost (MC) and marginal revenue (MR) are equal. Businesses can increase their revenues by starting to produce at this point. Profit maximisation is not, however, the only goal that businesses in real-world situations pursue.

2. The Profit-Maximising Rule (MC=MR):

According to the profit-maximising rule, businesses should produce at a level where marginal cost (MC) and marginal revenue (MR) are equal. Producing an additional unit would reduce revenues when MC is greater than MR. On the other hand, if MR surpasses MC, businesses should raise production to boost profits. This guideline aids businesses in making logical choices that will maximise their financial performance.

3. Divorce of Ownership from Control:

When shareholders, who own the company, give management the power to make decisions, ownership and control are separated. This is called the divorce of ownership and control. Owners and managers may have different goals as a result of this division. Managers could put their own interests ahead of just maximising shareholder value, such as job security or business expansion. The goals, behaviour, and performance of businesses may be affected by this agency problem. This is known as the principal agent problem.

Owners can offer incentives to help align objectives. For example, performance-related pay like bonuses can incentivise employees to try and make the company more profit. This is why in many sales jobs the company will pay you a base wage (usually not very good), coupled with a sales-related bonus (commission). This means the employee has a greater desire to perform and hit targets.

Another option available is to offer shares to the managers running the business. A share is a store of wealth. If a manager's wealth is stored as company shares, then the manager will want the company to do well because it affects him/her. There are many jobs where people in the top positions are required to hold shares in the company.

4. Alternative Objectives:

Firms can pursue a range of objectives beyond profit maximisation. These include:

- Survival: Surviving the current economic climate could be a priority for several businesses.

- Expansion: Businesses may concentrate on increasing their operations, market share, or product lines.

- Quality: Emphasising the creation of premium products or services to win over customers' trust and goodwill.

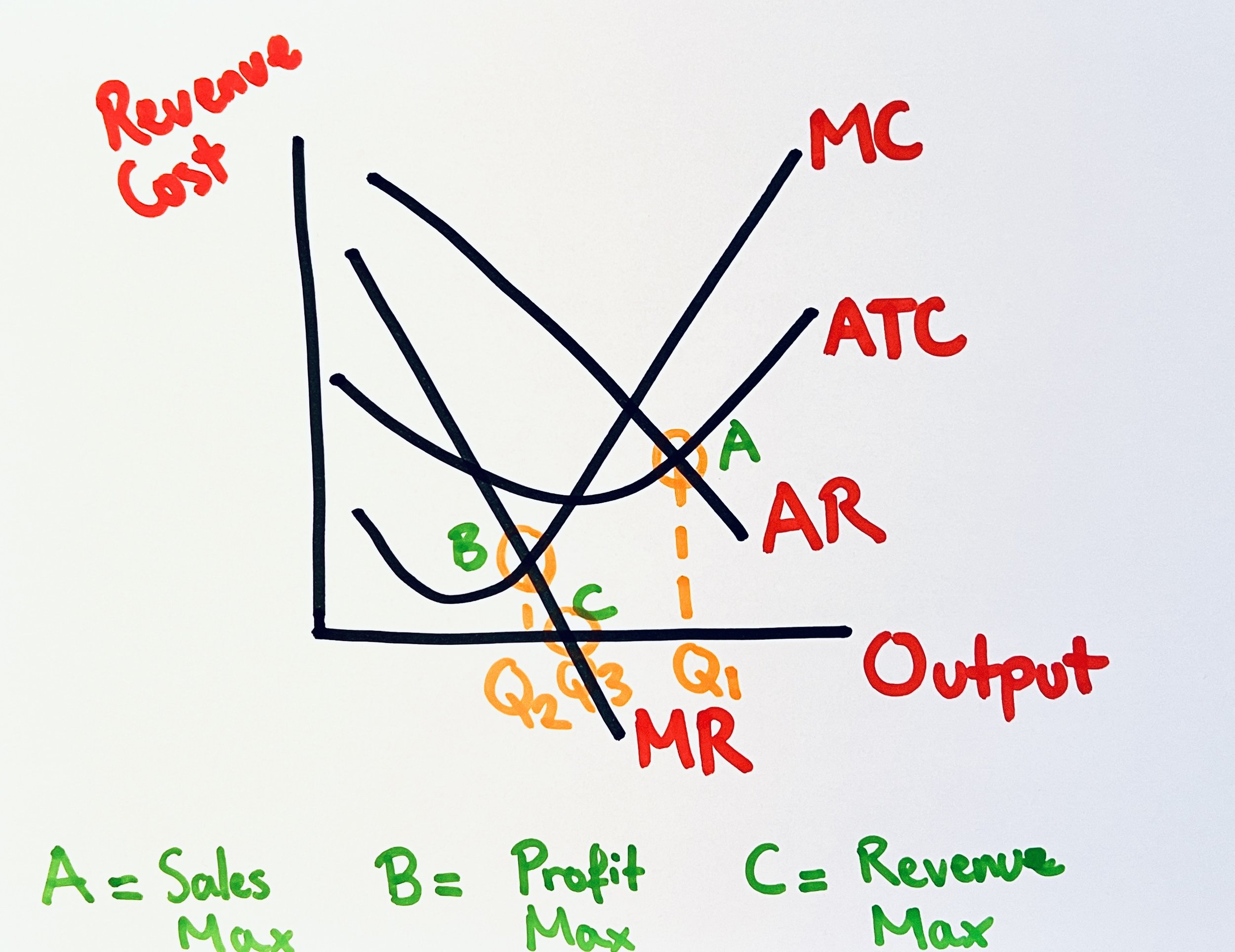

- Increasing Sales income: Aiming to increase overall income by adjusting production costs and prices. This typically occurs by decreasing prices. Sales maximisation occurs at the level where Price = Cost Per Unit. This is the same as Average Revenue = Average Cost.

- Increasing Market Share: Looking to win a larger share of the market by outperforming rivals or attracting more clients. Firms may do this by maximising their revenue. Revenue maximisation occurs at the point where Marginal Revenue = 0.

5. The Satisficing Principle:

According to the idea of satisficing, businesses should strive for acceptable results rather than the best possible ones. When faced with a variety of constraints and uncertainties, businesses may define goals that serve the needs of stakeholders while minimising unnecessary risks or expenses. Satisficing acknowledges the compromises businesses must make in order to strike a balance between several goals, including profit, client happiness, staff well-being, and social contribution.

6. Other Real-World Objectives

The most common real-world objective that's linked to profit will be profit margin.

A profit margin is a percentage-based target where profit is calculated as a percentage of the selling price. For example, if you sell a mug for £5 and your profit margin is 40%, then 40% of the price is profit e.g. £2 will be profit. The remaining £3 will be costs.

Another real-world objective is cost-plus pricing, also known as a mark-up. With this sort of pricing you calculate what your costs are first, and then you add a mark-up as a percentage. For example, if you are selling an Xbox and it costs £100 to produce, then if you add a 70% mark-up then your selling price will be £170. £70 is made as profit.

Conclusion:

Understanding a company's goals might help you better understand how they make decisions and behave. Profit maximisation is still a core idea, but it's important to understand that businesses have different goals and are subject to different restrictions. The divorce of ownership and control, alternate objectives, and the satisficing principle all help to illuminate the complexity of business behaviour and performance. Students can obtain a thorough understanding of the various factors that influence firms' behaviour in actual economic contexts by studying these ideas.

SUPPORTING DIAGRAMS

revenue/cost diagram to show profit max, sales max and revenue maximisation points